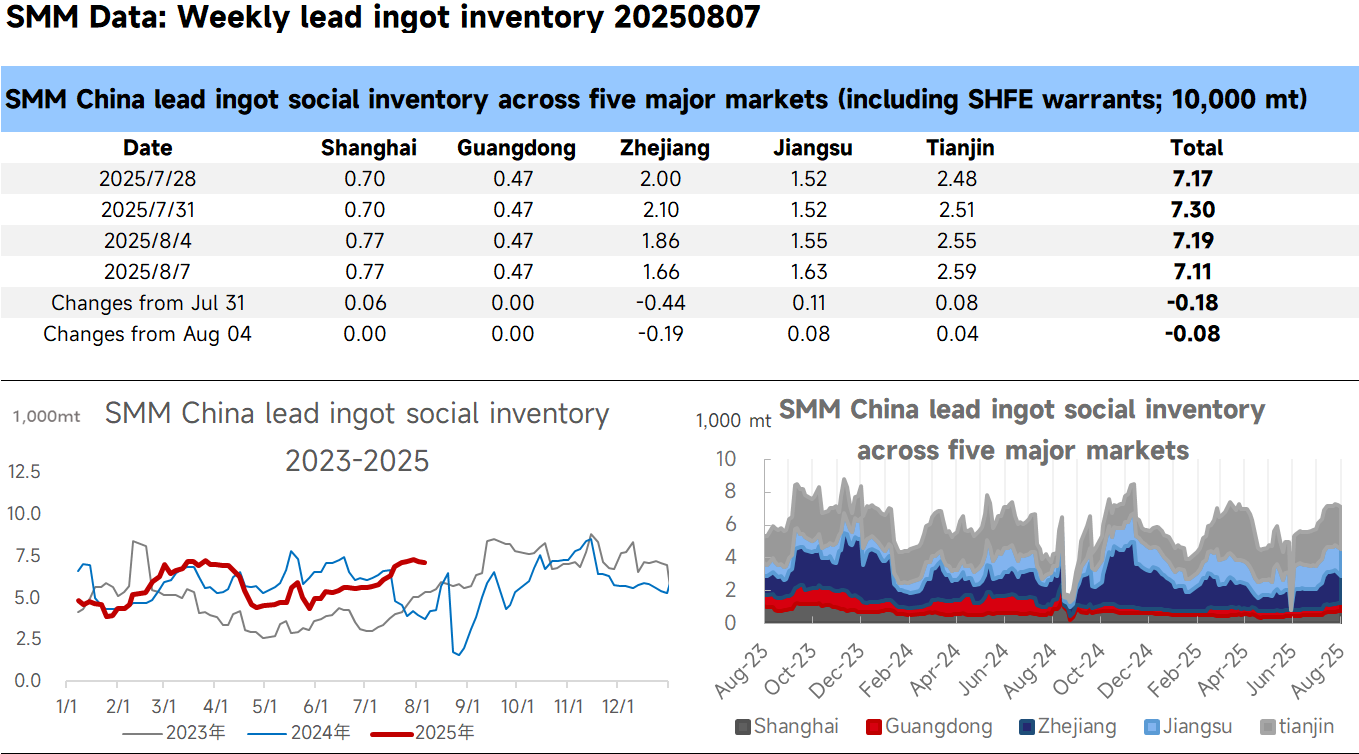

SMM News on August 7: According to SMM, as of August 7, the total social inventory of lead ingots across five regions monitored by SMM reached 71,100 mt, a decrease of 1,800 mt from July 31 and approximately 800 mt from August 4.

This week, production at primary lead smelters gradually resumed, while environmental protection inspections were underway in Anhui Province, leading to production constraints at some secondary lead enterprises and widening regional supply disparities for lead ingots. During this period, discounts for cargoes self-picked up from primary lead smelters narrowed, with mainstream production areas quoting prices at parity or a discount of 100-80 yuan/mt against the SMM #1 lead average price for factory delivery, or a discount of 100-80 yuan/mt against the SHFE lead 2509 contract. In contrast, warehouse cargoes in the Jiangsu, Zhejiang, Shanghai region were quoted at a discount of 50-20 yuan/mt against the SHFE lead 2509 contract. Some downstream enterprises opted for nearby procurement, leading to a decline in social warehouses of lead ingots. Recently, lead prices have oscillated and strengthened, with SHFE lead prices once approaching the 17,000 yuan/mt threshold. Downstream enterprises, wary of high prices, adopted a wait-and-see attitude, resulting in a decline in trading activity in the spot market. Next week, the SHFE lead 2508 contract approaches delivery, and there is a possibility of some lead ingots being transferred to warehouses before delivery. It is anticipated that the subsequent decline in social inventory of lead ingots may slow down.